However, if your credit history is borderline, you might wish to spend the cash to see if it is much better to apply now or wait till your score enhances. Your credit score can differ from one credit bureau to another, since some details (either positive or negative) might not be on all of your credit reports.

There are actually some very easy guidelines determining which credit history to utilize. the lower credit rating will be used. If you have a 700 credit history on Experian and a 680 on Equifax, the 680 score would be utilized. the middle rating will be used. If you have a 700 on Experian, 680 on Equifax and 660 on TransUnion, the 680 score would be utilized.

The lower credit report of the 2 debtors will be used. In basic, banks and home loan business wish to utilize the most affordable rating available because it will likely have actually taken into consideration all negative details that is readily available. You will not be able to hide from unfavorable details on your credit report when getting a home loan.

According to Timothy Mayopoulos, the Fannie Mae CEO, "some people suggest we slavishly follow FICO. That is not real. We evaluate credit information through own automated system and form our own judgments about the credit reliability." In addition to the FICO credit history, there are a number of underwriting rules being utilized.

With trended data, loan providers will have a various view of your payment history. In particular, loan providers will see if you pay your credit card balance completely monthly or not. People who borrow on their charge card are, in general, considered as much riskier than individuals who utilize their cards but pay the balance in full every month.

So, if you have an excellent rating (since of low usage) however never ever pay your balance in complete, you might find it more challenging or more expensive to get a home mortgage. All of this information can seem intimidating. However my recommendations stays simple. Just spend on your credit card what you can manage to pay off completely and on time each month.

What Are The Lowest Interest Rates For Mortgages - Questions

If you do those two things consistently in time, you will likely qualify for the best deals at any loan provider. If you are not applying for a Fannie Mae or Freddie Mac mortgage, the credit rating is most likely at the discretion of the lending institution. For example, a bank may have a Jumbo Home mortgage item that will be maintained by itself balance sheet.

You can definitely ask your loan officer beforehand what credit report the bank utilizes to make choices. However it will differ. Banks usually utilize some version of FICO in their underwriting choices. Nevertheless, it could be variable in the scoring design, or it could be utilized in a decision matrix in addition to a custom-made score or other guidelines.

FICO 8 is a credit-scoring system released in 2009. Because then, just a few loan providers have adopted it. The large bulk of lending institutions still depend on FICO 2, 4, and 5 ratings, which are all part of a larger report mortgage loan providers can acquire called the property home loan credit report (RMCR).

(EFX), Experian PLC (EXPN) and TransUnion (TRU). Home loan loan providers generally take the middle rating from this report. For instance, if your credit ratings from the above companies are 710, 690, and 610, the lending institution generally makes its choice based on the 690 score. However, more loan providers are most likely to move to FICO 8, so it is crucial to understand the five reasons it makes ball game various: FICO 8 is more delicate to highly-used credit cards.

FICO 8 is more lenient to separated late payments, but regular late payments are punished more. FICO 8 is more careful with, and more sensitive to, licensed users on charge card. Small-balance delinquencies of under $100 are overlooked. Consumers are divided into a lot more categorical profiles under FICO 8.

Through April 20, 2021, Experian, TransUnion and Equifax will offer all U.S. consumers totally free weekly credit reports through AnnualCreditReport. com to help you protect your financial health throughout the unexpected and extraordinary difficulty triggered by COVID-19. If you plan to purchase a home in the coming year, taking actions now to beautify your credit profile can increase your chances of getting approved for a home mortgage and minimize the quantity of interest you'll be charged on the loan.

Not known Details About What Is The Current Interest Rate For Commercial Mortgages

When you send a mortgage application, they'll inspect your credit reports preserved by one or more of the three national credit bureaus (Experian, TransUnion and Equifax), and the credit history stemmed from those reports. Lenders utilize credit info to help decide whether they want to provide you a home loan and, if so, just how much they're ready to provide you and just how much they'll charge you in interest.

The very first action in prepping your credit for a home loan is discovering where your credit presently stands. That means inspecting your ratings, and getting your credit reports from all three credit bureaus (Experian, TransUnion and Equifax) to examine the elements affecting them. You can get a totally free credit report from Experian, Equifax and TransUnion at AnnualCreditReport.

Evaluation each credit report carefully to make sure it precisely reflects your credit rating - what does ltv stand for in mortgages. If you get all 3 reports at the same time, don't be shocked if there are minor distinctions in between https://www.liveinternet.ru/users/legonaxl50/post480800248/ them. Your loan providers may not report all of your accounts to every credit bureau, or may send updates to the how to get rid of timeshare credit bureaus on somewhat various schedules.

Here are some things to look for when you get your reports: High account balances relative to your credit limitations. Paying for your balances will help your credit history. Past-due accounts, charge-offs and accounts in collections. If possible, bring all accounts current and settle any outstanding collection accounts. Loans or charge account that shouldn't be there (which might show criminal activity), and payments improperly noted as late or missed.

At the same time you're checking your credit reports, it's a great concept to have a look at your FICO Rating (which Helpful site you can get for complimentary from Experian and other companies). A credit report distills the contents of your credit report into a three-digit number, so if there are enhancements made in your reports, your rating will likely increase when that info is reported to the credit bureaus.

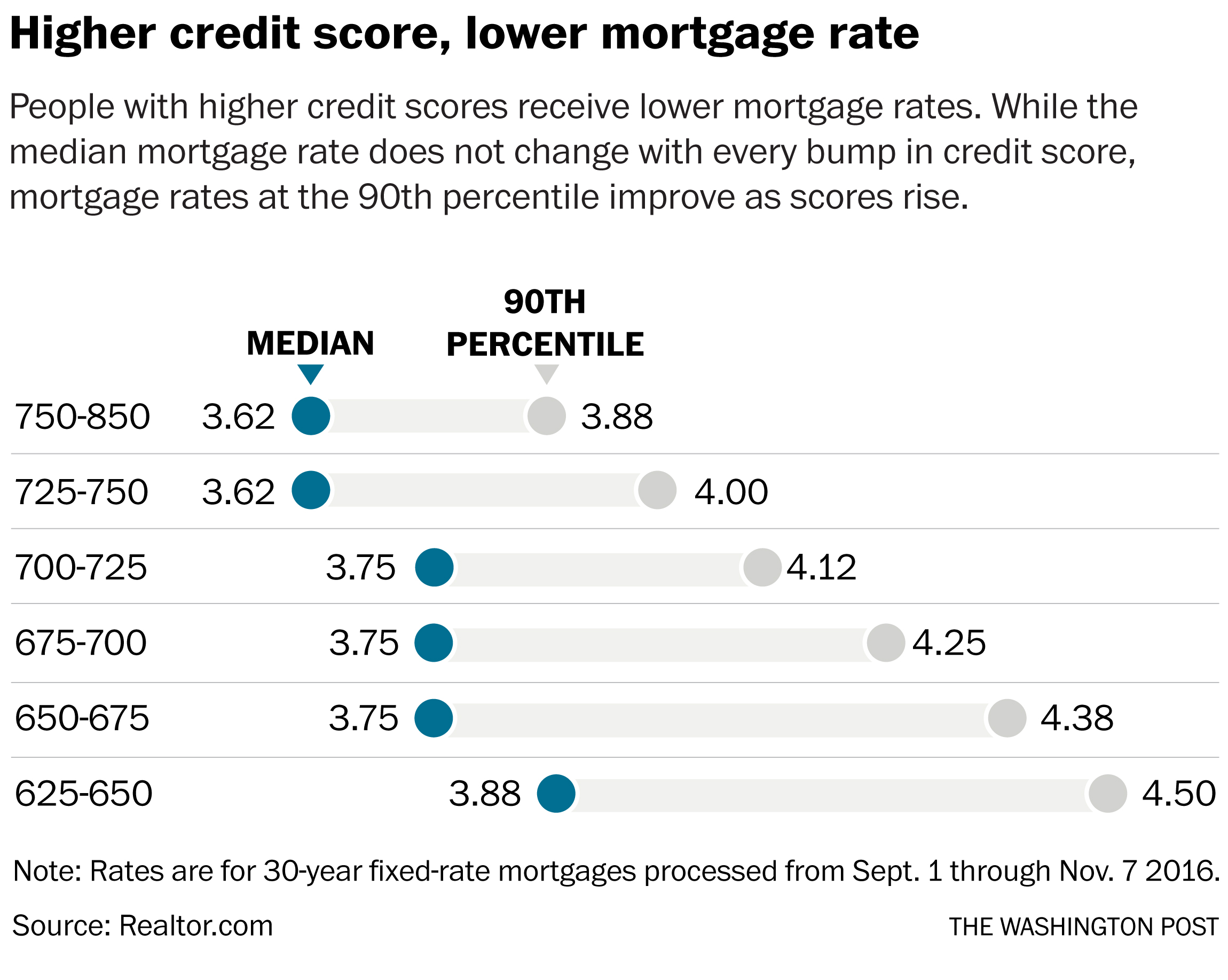

Lenders likewise use credit rating to help set the rates of interest they charge, with higher credit scores usually equating into lower interest rates. For instance, say you begin with a FICO Score of 675. According to the FICO Loan Cost Savings Calculator, you could buy a $300,000 home with a 20% down payment (total loan quantity of $240,000) and qualify for a 30-year fixed mortgage with a rate of interest of about 3.

The Basic Principles Of What Are The Lowest Interest Rates For Mortgages

Improving your rating just a couple of points, to 680 or more, might qualify you for an interest rate of 2. 83% conserving you almost $10,000 ($ 9,924) over the life of the loan. Bringing your rating approximately 700 might land you a rate of about 2. 65%, saving you an extra $18,000.